Introduction

Streaming now accounts for 84% of recorded music revenue in markets like the United States, making it the primary income source for artists worldwide. Yet many independent artists struggle to understand how platform algorithms work, where their listeners come from, and how to maximize revenue across multiple services.

These platforms have replaced physical sales and downloads entirely. They've reshaped how artists distribute music, how listeners discover new tracks, and how royalties flow back to creators.

For artists, labels, and distributors, understanding global streaming trends means knowing where to focus distribution efforts, which markets offer growth potential, and how algorithmic discovery and mobile-first consumption patterns impact revenue models.

TL;DR

- Global music streaming market projected to reach $43.9 billion USD by 2034 at 7.46% CAGR

- Emerging markets in Asia Pacific, Latin America, and Africa are growing at 22%+ annually as smartphone penetration expands

- AI-powered playlists drive 66% of streams, reshaping how listeners discover music

- Independent artists now hold 29.7% of market share via DIY distribution platforms

- 84% of Billboard Global 200 entries in 2024 had TikTok virality first, proving social media is now the primary discovery engine

The Rise of Independent Artist Empowerment Through DIY Distribution

Independent artists are bypassing traditional label gatekeepers through digital distribution platforms. These platforms offer 95-100% royalty retention, global streaming access, and transparent analytics—fundamentally shifting power from labels to creators.

Market Share and Growth

The independent sector is outpacing major labels. In 2024, non-major labels increased their market share to 29.7%, with revenues climbing 8.2% to $10.7 billion. The "Artists Direct" segment—self-releasing artists—generated $2.0 billion, growing 4.7% year-over-year, with the population of these artists reaching 8.2 million.

In streaming specifically, independent artists grew revenues by 8.4% to $5.4 billion, outperforming the 5.4% growth rate of major labels. This momentum reflects fundamental changes in how artists access audiences and monetize their work.

Why This Matters

Key Drivers of Independent Empowerment

- Royalty retention: Platforms allow artists to keep 85-100% of streaming royalties versus traditional label deals offering 15-25%

- Global reach: Instant access to all major streaming platforms (Spotify, Apple Music, Amazon Music, YouTube Music) without label infrastructure

- Transparent analytics: Real-time data on streams, audience demographics, and geographic performance

- Professional tools: Access to Dolby Atmos distribution, YouTube Content ID, and automated royalty splits at source

Platforms like Madverse enable independent artists to retain ownership while accessing professional-grade distribution tools previously available only through major labels. Artists get spatial audio distribution, sync licensing opportunities for TV and film, and editorial playlist pitching services—all while keeping 95% of royalties.

Beyond Economics

This distribution model gives independent artists control over their creative output, release schedules, and fan relationships without middlemen. This shift has created a more diverse musical landscape where niche genres and regional sounds can find global audiences without conforming to major label formulas.

Mobile-First Consumption and Emerging Market Explosion

Mobile devices have become the primary gateway to music streaming, particularly in emerging markets where smartphones represent the first and often only internet-connected device.

This mobile-first shift is driving explosive growth in regions that will define the industry's future.

Connectivity Infrastructure

Global mobile broadband has reached 6 billion users (74% of the global population), while 5G connections hit 1.6 billion and are projected to reach 5.5 billion by 2030. This infrastructure expansion enables high-fidelity streaming on mobile devices without buffering, supporting the shift toward premium audio formats.

Regional Growth Hotspots

The fastest-growing streaming markets are all in emerging regions:

| Region | 2024 Growth Rate | Key Driver |

|---|---|---|

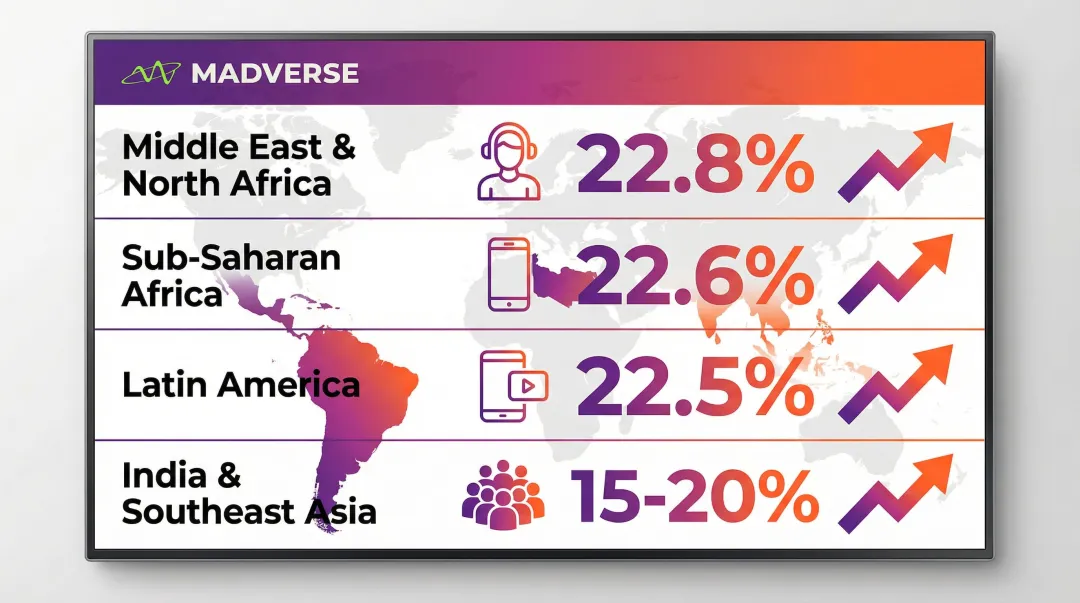

| Middle East & North Africa | +22.8% | Youth demographics, affordable data plans |

| Sub-Saharan Africa | +22.6% | Smartphone penetration, regional platforms like Boomplay |

| Latin America | +22.5% | Mobile-first consumption (streaming = 87.8% of revenue) |

| India & Southeast Asia | +15-20% | Massive population, low-cost data plans |

In MENA, streaming accounts for 99.5% of music revenues, demonstrating how mobile-first markets skip physical and download eras entirely. Latin America shows similar patterns, with streaming representing 87.8% of regional revenues.

Regional Platform Competition

While global platforms dominate, region-specific services capture significant local market share:

- NetEase Cloud Music (China): Localised content libraries, social features, and government compliance

- Boomplay (Africa): Offline listening for limited connectivity, local artist focus

- Regional Latin platforms: Partnerships with telecom providers for bundled data

These markets represent the future majority of streaming users. By 2030, emerging markets will account for more than half of global streaming revenue growth.

This growth stems from youth demographics, affordable data plans, and local content that resonates with regional audiences.

AI-Powered Personalization and Discovery Revolution

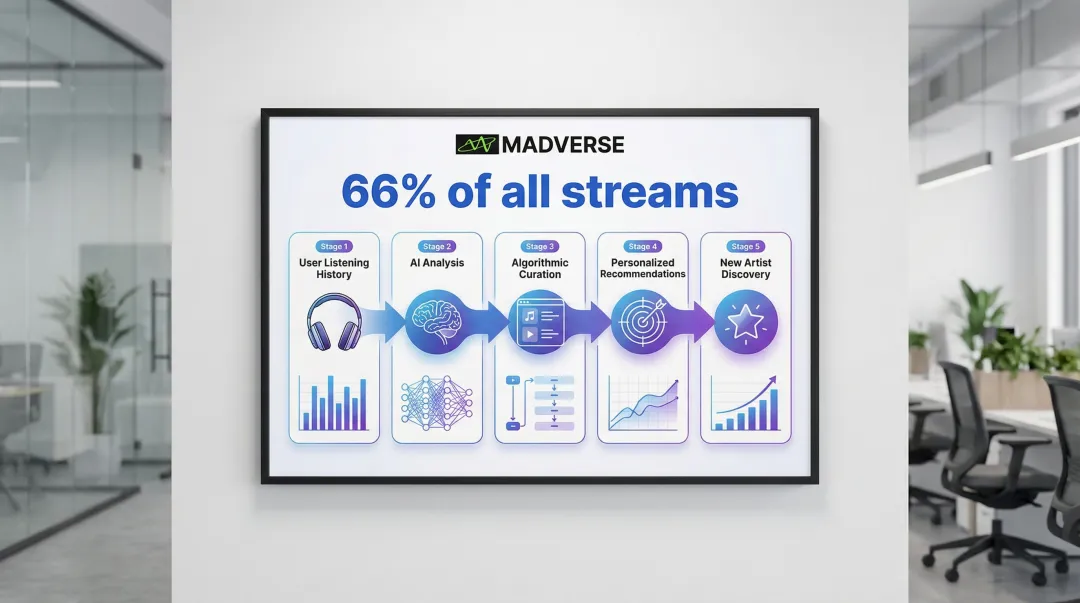

Artificial intelligence has fundamentally transformed music discovery, shifting control from user-initiated searches to algorithmic curation.

This revolution impacts both listener experience and artist visibility, creating new pathways to success while raising questions about discoverability.

Algorithmic Dominance

Research shows that 66% of streams now originate from algorithmic playlists, compared to 34% from user searches. This means two-thirds of listening happens through AI-curated recommendations rather than deliberate user choice.

Spotify's "Discover Weekly" exemplifies this shift:

- Generated over 100 billion streams since launch

- Creates 56 million new artist discoveries every week

- 77% of discoveries are for emerging artists, not established names

AI Applications Across the Value Chain

These algorithms don't just drive listener behavior—they reshape how the entire industry operates.

For listeners:

- Personalized daily mixes based on listening history and mood

- Context-aware recommendations (workout, study, commute playlists)

- Predictive "Release Radar" featuring new music from followed artists

For artists and distributors:

- Audience targeting for promotional campaigns

- Release timing optimization based on listener behavior patterns

- Playlist placement predictions and submission optimization

- Automated mastering services using machine learning

Impact on Artist Strategy

AI-driven discovery has created new priorities for artists:

- Consistent release cadence: Algorithms favor artists who release regularly, maintaining visibility in recommendation feeds

- Data-driven decisions: Understanding which tracks generate playlist adds and completion rates

- Genre fluidity: AI identifies micro-genres and connects artists to niche audiences globally

The challenge: artists must balance creating authentic music with understanding the signals that trigger algorithmic promotion.

Those who master this balance—releasing quality music consistently while leveraging data insights—gain disproportionate visibility in a crowded market.

Multi-Format Integration: Audio, Video, and Social Convergence

Streaming services have evolved beyond pure audio platforms.

The convergence of audio streaming, video content, and social features has created unified ecosystems where discovery, consumption, and community happen simultaneously. Artists now reach audiences across multiple formats within single platforms.

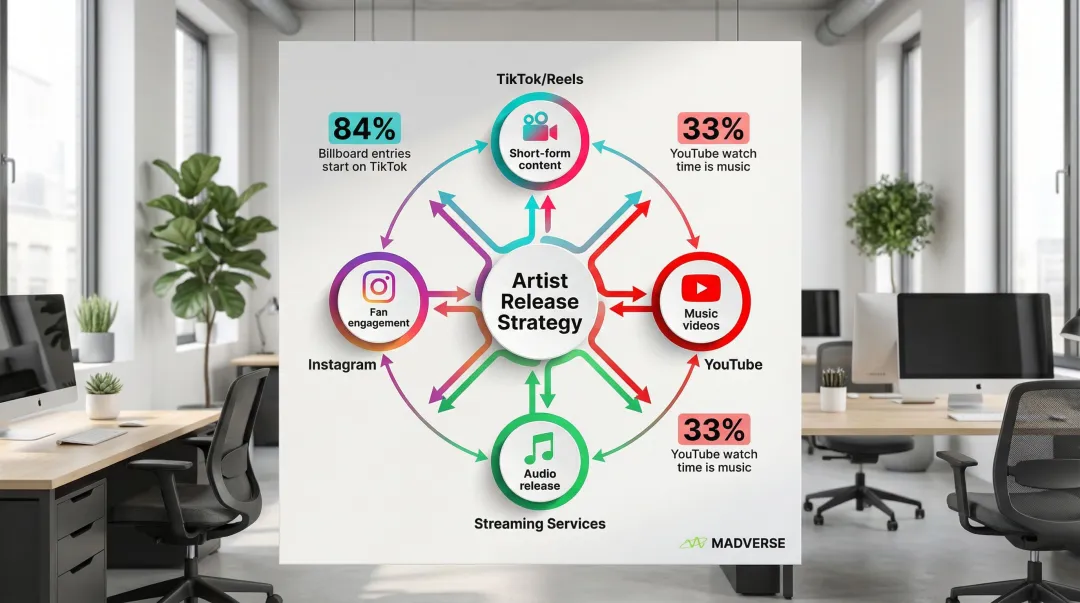

TikTok's Chart Dominance

84% of all songs that entered the Billboard Global 200 in 2024 had a viral TikTok moment first. In 2025, 8 out of 10 Billboard #1 songs were preceded by TikTok virality. This represents a fundamental shift: social virality is now a requirement for mainstream success, not a bonus.

TikTok's "Add to Music App" feature has generated over 3 billion track saves to streaming services, creating a direct pipeline from short-form video discovery to streaming consumption.

Multi-Platform Ecosystem

YouTube's dual role:

- Music accounts for 33% of all YouTube watch time

- YouTube Music has surpassed 100 million paid subscribers

- Acts simultaneously as discovery platform (music videos, lyric videos) and streaming service

Instagram integration:

- Reels now account for 35% of time spent on Instagram, with 2 billion monthly active users

- Stories music features drive discovery through user-generated content

- Artists leverage Instagram for direct fan communication alongside music promotion

Strategic Implications

This multi-platform landscape demands coordinated strategies across formats. Successful artists now require:

- Short-form video content optimized for TikTok/Reels algorithms

- Music video releases synchronized with audio streaming launches

- Social engagement through behind-the-scenes content, challenges, and fan interaction

- Cross-platform coordination ensuring visual and audio content amplify each other

Distribution platforms now support synchronized releases across audio streaming services, video platforms (VEVO, Apple Music, Tidal), and social networks to maximize viral potential through coordinated multi-format launches.

What This Means for Artists:

- Audio quality alone no longer guarantees success

- Visual storytelling has become non-negotiable

- Social media presence directly impacts streaming performance

- Community building drives long-term audience retention

Evolving Revenue Models and Artist Economics

Streaming economics are in flux as platforms experiment with hybrid models, user-centric payment systems, and creator monetization tools. Understanding current payout structures and emerging alternatives is critical for artists and labels planning long-term strategies.

Current Payout Landscape

Per-stream rates vary significantly by platform and business model:

| Platform | Payout Per Stream | Business Model |

|---|---|---|

| Tidal | $0.01284 | Premium HiFi focus |

| Apple Music | $0.008 | Subscription-only, +10% for Spatial Audio |

| Amazon Music | $0.00402 | Mixed (standalone + Prime bundle) |

| Spotify | $0.003-$0.005 | Freemium (ad-supported + premium) |

| YouTube Music | $0.002 | Ad-supported + premium |

Apple Music introduced a royalty structure that pays up to 10% higher royalties for content available in Spatial Audio (Dolby Atmos), regardless of whether users listen to that specific version. This incentive drove a 5,000% increase in Spatial Audio catalog availability.

Subscription vs. Ad-Supported Growth

In the US, paid subscriptions generated ₹9.74 lakh crore ($11.685 billion) in 2024, growing 4.6%, while ad-supported revenue declined 1.8% to ₹1.53 lakh crore ($1.83 billion).

The total number of users on paid subscription accounts reached 752 million globally in 2024, a 10.6% increase year-over-year.

Emerging Payment Models

Beyond traditional pro-rata distribution, the industry is exploring new approaches to artist compensation.

User-centric payment systems (fan-powered royalties) redirect subscription fees to the artists each subscriber actually listens to, rather than pooling all revenue and distributing pro-rata. SoundCloud pioneered this model, though major platforms have been slow to adopt.

Hybrid features gaining traction:

- Direct artist tipping and support features

- Transparent royalty splitting at source (not post-collection)

- Advance tracking for artists with advances

- Real-time payment reporting replacing quarterly statements

Distribution platforms now offer automated royalty splits at source, allowing collaborators to receive their share directly without manual distribution. For independent artists choosing between distributors, this transparency has become a deciding factor—platforms like Madverse that provide real-time splits and retain 95% of royalties attract artists who previously might have signed traditional deals.

Economic Reality for Artists

To earn minimum wage from streaming alone, an artist needs millions of streams monthly. This reality drives artists toward diversified strategies:

- Merchandise, live performances, sync licensing, and direct fan support

- Building deep catalogs that generate passive streaming income

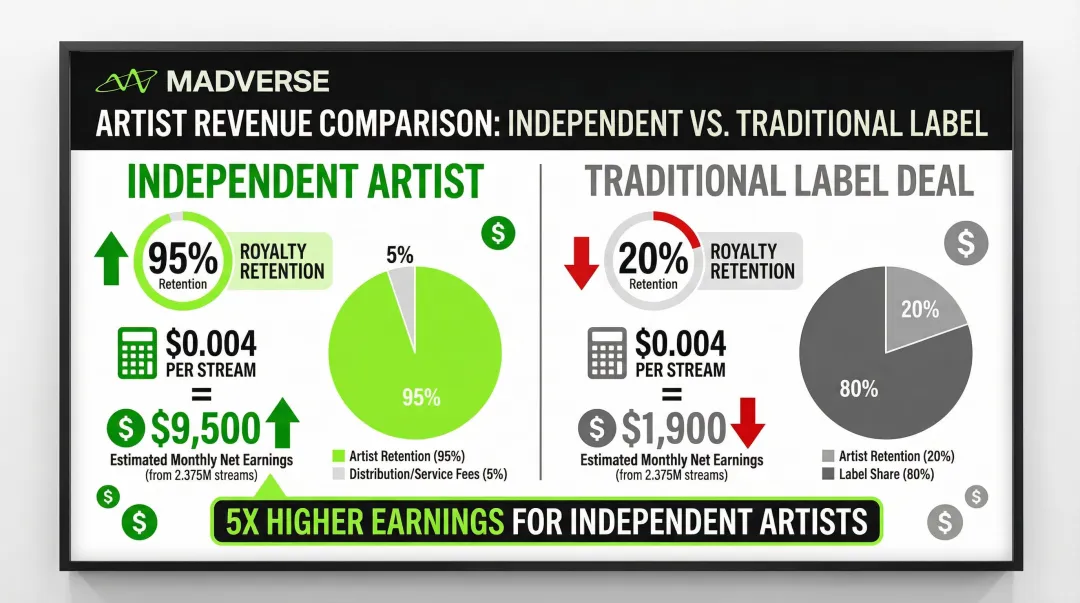

- Choosing distributors offering 95-100% royalty retention versus traditional 85% or lower

The economics favor independent artists who retain ownership and control distribution costs.

An artist keeping 95% of $0.004 per stream earns significantly more than an artist on a traditional label deal keeping 20% of $0.004 per stream.

What's Driving These Music Streaming Trends

Multiple converging forces are accelerating the transformation of music streaming, from technological infrastructure to shifting consumer expectations and competitive dynamics.

Technology Infrastructure

Three infrastructure advances are removing barriers to streaming adoption:

- 5G connectivity: With 1.6 billion 5G connections globally, expanding to 5.5 billion by 2030, high-fidelity and spatial audio streaming on mobile devices becomes seamless, particularly in emerging markets where premium formats were previously inaccessible

- Cloud infrastructure: Scalable platforms enable services to deliver billions of streams daily while powering AI recommendation engines that process massive datasets in real-time

- Affordable smartphones: Device costs have dropped dramatically in emerging markets, with capable streaming devices now available for under ₹8,350 ($100)

Consumer Behavior Shifts

Streaming now accounts for 69.0% of global recorded music revenues, with 84% in the US market. This represents a fundamental shift from ownership (downloads, CDs) to access (streaming subscriptions).

Driving factors:

- On-demand expectations: Consumers expect instant access to entire catalogs, not individual purchases

- Discovery over curation: Listeners prefer algorithmic discovery to building personal libraries

- Mobile-first consumption: Music listening increasingly happens during commutes, workouts, and multitasking rather than dedicated listening sessions

Competitive Dynamics

As the market matures, platforms are competing on multiple fronts beyond catalog size:

- Audio quality tiers: Lossless audio (Apple Music, Tidal, Amazon Music HD) and spatial audio formats

- Exclusive content: Platform-exclusive releases, podcasts, and live sessions

- Pricing experiments: Family plans, student discounts, bundled services (Amazon Prime, Apple One)

- Artist-friendly features: Higher payouts for premium formats, transparent analytics, promotional tools

This competitive landscape increasingly favors artists. The creator economy explosion has shifted platform strategy from pure listener acquisition to creator retention, with streaming services now competing to attract artists through better tools, higher payouts, and transparent economics—a trend that directly benefits independent artists using distribution services to reach multiple platforms simultaneously.

How These Trends Are Impacting the Music Streaming Industry

Music streaming's transformation is reshaping how the industry operates. From release strategies to hiring priorities, platforms and artists are adapting to new realities across three key dimensions: operations, business models, and workforce needs.

Operational Impact

Streaming algorithms have fundamentally changed how music reaches listeners:

- Shorter release cycles: To maintain algorithmic visibility, artists now release music more frequently. The population of self-releasing artists reached 8.2 million in 2024, collectively releasing millions of tracks annually.

- Data-driven A&R: Labels use AI tools like Sodatone (acquired by Warner Music Group) and Instrumental to identify trending tracks on TikTok or Spotify before signing artists, shifting focus to tracks with demonstrated streaming growth rather than traditional scouting.

- Automated distribution workflows: Artists upload tracks, set release dates, and distribute to 100+ platforms through single interfaces. Real-time analytics replace months-long reporting cycles, enabling rapid strategy adjustments.

- Quality format requirements: With Apple paying 10% premiums for Spatial Audio, artists and distributors are investing in Dolby Atmos mixing and mastering, creating new technical requirements for competitive releases.

Business Impact

The economics of music distribution are shifting toward artist empowerment:

- Investment in emerging markets: Labels and platforms are expanding infrastructure in Latin America, Africa, and Asia Pacific—including India and South Asia—where growth rates exceed 20% annually through localized content libraries, regional partnerships, and affordable pricing tiers.

- Acquisition of distribution companies: Major labels are acquiring DIY distribution platforms to capture independent artist revenue without traditional A&R investment, aiming to monetize the independent sector's growth.

- Direct-to-artist services: Platforms increasingly offer artist-facing tools like analytics, promotional credits, and playlist pitching to compete for creator loyalty. Services like Madverse exemplify this shift, providing independent artists with professional distribution infrastructure while allowing them to retain up to 95% of royalties.

- Transparent royalty systems: Distributors emphasize transparent reporting, automated payment splits, and higher retention rates as competitive advantages to attract independent artists who demand visibility into their earnings.

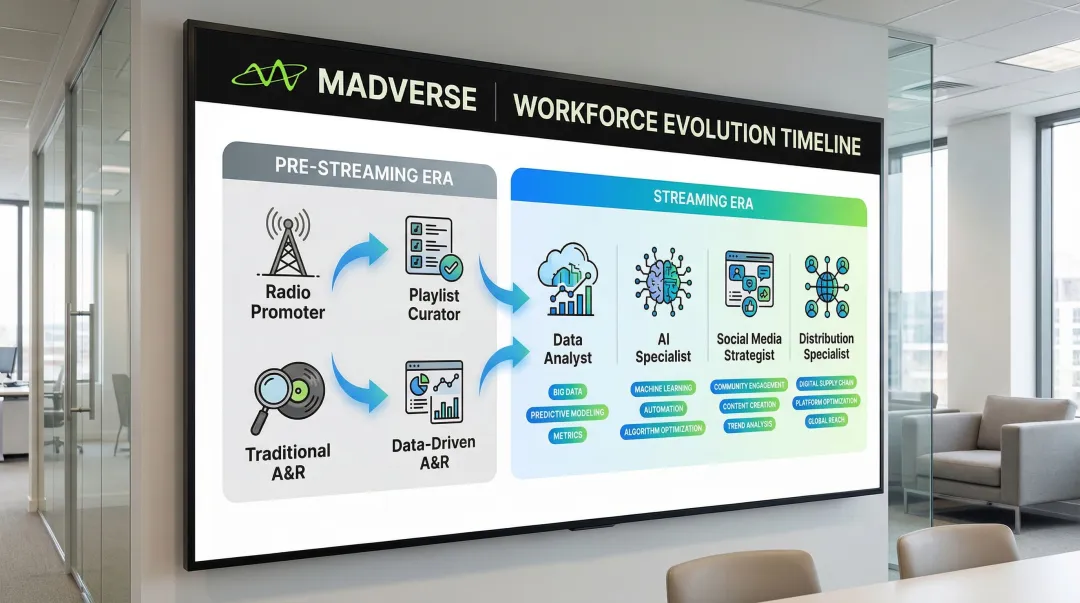

Workforce Impact

The streaming era is creating new roles while transforming existing ones:

| Role Type | Key Responsibilities | Skills Required |

|---|---|---|

| Playlist curators (New) | Navigate ecosystems where 66% of streams are algorithmic or playlist-driven | Music curation, platform algorithms, listener behavior analysis |

| Data analysts (New) | Interpret consumption data from platforms like Spotify for Artists to inform marketing and release strategies | Analytics tools, trend identification, strategic planning |

| AI specialists (New) | Leverage machine learning for mastering, marketing targeting, and audience segmentation | Machine learning, audio engineering, audience modeling |

| Social media strategists (New) | Create and optimize short-form video content for TikTok and Instagram discovery | Video production, platform algorithms, content virality |

| A&R executives (Evolved) | Combine traditional talent scouting with data analysis, identifying artists with streaming momentum | Talent evaluation, data interpretation, industry relationships |

| Radio promoters (Evolved) | Shift focus to playlist pitching and algorithmic optimization as radio's influence declines | Playlist relationships, platform knowledge, digital promotion |

| Marketing teams (Evolved) | Coordinate multi-format campaigns across audio streaming, video platforms, and social networks | Digital marketing, cross-platform strategy, content coordination |

Industry employers now prioritize digital fluency, data literacy, and social media expertise alongside traditional music industry knowledge.

Future Signals for Music Streaming Services Through 2033

The streaming landscape will continue evolving rapidly through 2033. From blockchain royalty systems to AI-generated radio, several emerging technologies and business models are reshaping how artists earn and listeners discover music.

Technologies to Watch

Blockchain-based royalty tracking: While current blockchain platforms like Audius have only ~6 million monthly users compared to Spotify's hundreds of millions, the technology offers potential for transparent, automated royalty distribution. Future applications may focus on "smart contract royalties" that eliminate intermediaries in payment chains.

Immersive audio formats: With 90% of Apple Music listeners having experienced Spatial Audio and 80% of the Global Daily Top 100 available in the format, Dolby Atmos is becoming the industry standard. By 2030, spatial audio may be the default format for new releases.

Voice-activated listening: As smart speakers and voice assistants grow, voice-initiated streaming ("Play something I'll like") shifts discovery entirely to AI, further reducing user-initiated search.

AI-generated personalized radio: Future AI may create unique "radio stations" for each listener, mixing catalog tracks with real-time remixes and mashups tailored to individual taste profiles.

These technological shifts point toward broader structural changes in how streaming platforms operate and compensate artists.

Potential Industry Scenarios (2030-2033)

Several competing scenarios may define the industry landscape:

Platform consolidation: The market may consolidate around 3-4 global platforms (Spotify, Apple Music, YouTube Music, Amazon Music) as smaller services struggle with content costs and competition. However, niche platforms serving specific genres or communities could thrive.

User-centric payment models: Pressure from artist advocacy groups may push major platforms toward fan-powered royalty systems, where subscription fees flow to artists each subscriber actually listens to rather than pro-rata pooling. Services like Madverse already enable royalty splits at source, suggesting this model's viability for independent distribution.

Regulatory intervention: Governments may mandate minimum per-stream rates or transparency requirements, particularly in the EU, reshaping platform economics and potentially reducing profit margins. Per-stream rates vary significantly by region, with markets like India showing different economics than Western markets.

Genre-specific platforms: Community-owned or genre-focused streaming services (jazz, classical, hip-hop) may emerge as alternatives to algorithm-driven mainstream platforms, offering curated experiences for dedicated fans.

Direct-to-fan integration: Streaming platforms may integrate direct fan support features (tipping, subscriptions, exclusive content access) more deeply, creating hybrid models where streaming and patronage coexist.

The most likely outcome combines several of these trends. Major platforms will continue dominating while gradually adopting user-centric payment elements. AI sophistication in discovery will increase significantly. Emerging markets will show persistent growth as they approach mature market penetration rates.

Conclusion

Music streaming continues reshaping how artists create, distribute, and monetize their work worldwide. The market's projected growth to ₹36 lakh crore by 2034 reflects streaming's permanent position as the industry's economic engine.

Key global trends driving this growth:

- Independent artist empowerment through DIY distribution

- Mobile-first consumption in emerging markets

- AI-powered personalization and discovery

- Social media integration expanding reach

- Evolving revenue models beyond traditional streams

Artists and labels who adapt early gain competitive advantage. This means leveraging platforms like Madverse that offer 95% royalty retention, utilizing data analytics for release optimization, and executing multi-format strategies across audio, video, and social channels. The independent sector's capture of nearly 30% market share demonstrates that major label backing is no longer a prerequisite for streaming success.

Understanding regional growth dynamics, algorithmic discovery mechanics, and emerging payment models will position artists to take advantage of opportunities as streaming evolves through 2033. Success belongs to those who stay informed and adapt quickly.

Frequently Asked Questions

Which music streaming app is the most used?

Spotify leads globally with 290 million paid subscribers as of Q4 2025, followed by Apple Music, Amazon Music, and YouTube Music. Regional leaders include NetEase Cloud Music (China) and Boomplay (Africa).

How many people use music streaming apps?

Over 752 million people subscribe to paid streaming services as of 2024, growing 10.6% annually. Including ad-supported users, total reach exceeds 1.5 billion globally.

Which app is the best for music distribution?

The best distributor depends on your needs. Popular options include DistroKid, TuneCore, CD Baby, and Madverse. Key factors: royalty retention (95-100% is optimal), payment splits, platform reach, and tools like Dolby Atmos and YouTube Content ID.

What are the fastest growing music streaming markets?

Asia Pacific (India, Southeast Asia, China), Latin America (Brazil +21.7%, Mexico +15.6%), and Africa lead with 20%+ annual growth. This expansion is driven by smartphone adoption, affordable data, and mobile-first youth demographics.

How much do artists earn from streaming in 2033?

Payouts range from $0.002-$0.01284 USD per stream. Earnings depend on stream count, distribution terms (retaining 85-100% of royalties), and bonuses like Apple Music's Spatial Audio premium. High royalty retention and direct splits maximize revenue.

What is the difference between music streaming and music distribution?

Music streaming refers to platforms where listeners consume music (Spotify, Apple Music, YouTube Music). Music distribution refers to services that deliver artists' music to those streaming platforms (DistroKid, Madverse, TuneCore). Distributors act as intermediaries, handling technical delivery, metadata management, and royalty collection from streaming services.